Applying for a loan online in India has become remarkably easy. A borrower can discover an offer, upload documents, complete verification and receive a lending decision without visiting a bank branch.

But speed created new risks too: unclear charges, misleading “instant loan” claims, excessive access to phone data, confusing relationships between lending apps and actual lenders, and repayment journeys in which borrowers did not always know whom they were paying.

The regulatory direction from the Reserve Bank of India is designed to make digital lending more transparent, accountable and borrower-centric. The framework has evolved from the 2022 digital lending guidelines into the consolidated Reserve Bank of India (Digital Lending) Directions, 2025, which form the key regulatory foundation borrowers encounter in 2026.

For borrowers, the practical message is simple: a legitimate digital loan journey should make it easier to understand who is lending the money, what the loan really costs, what data is being collected, how repayment works and where to complain if something goes wrong.

This guide explains what those protections mean for salaried employees, self-employed professionals and MSMEs—and how to use them before accepting your next loan.

What Changed in Digital Lending?

The biggest change is not a single rule. It is a shift in how the entire digital lending journey is expected to work.

Earlier, borrowers often focused on three questions:

How much can I borrow?

What is the EMI?

How quickly will I receive the money?

Those questions are still relevant, but they are no longer enough.

A careful borrower should now also ask:

Who is the actual regulated lender?

What is the Annual Percentage Rate, or APR?

What fees are included in the total borrowing cost?

Have I received a Key Fact Statement?

What data permissions am I giving?

Where will the loan be disbursed?

Where will I make repayments?

Is there a cooling-off period?

Who handles complaints?

What happens if I miss an EMI?

The regulatory framework puts responsibility on regulated lenders for digital lending arrangements involving their lending service providers. RBI's digital lending FAQs also clarify that a regulated entity remains responsible for resolving complaints arising from the actions of the lending service providers it engages.

That matters because the company or app through which you discover a loan may not always be the institution actually lending the money.

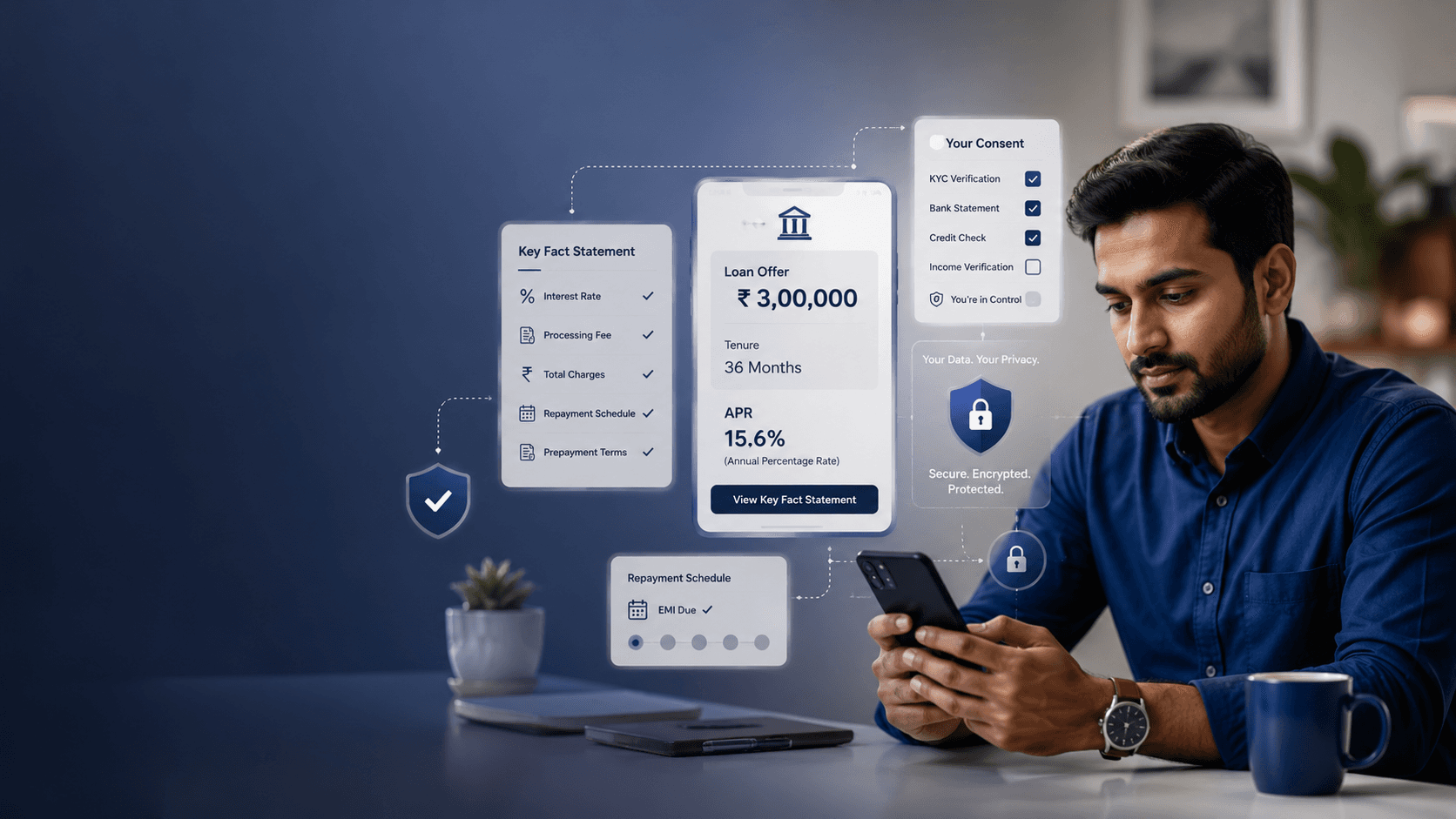

The Key Fact Statement Is Now One of Your Most Important Documents

The Key Fact Statement (KFS) is designed to solve a basic problem: borrowers should be able to understand and compare a loan before committing to it.

Think of the KFS as the loan's decision sheet.

Instead of forcing you to search through a long agreement for scattered information, the KFS brings critical terms together in a standardised format. RBI has progressively strengthened KFS requirements, with the objective of giving borrowers a concise view of key loan terms and costs.

A borrower should review, at minimum:

sanctioned loan amount;

loan tenure;

interest rate and its nature;

APR;

repayment schedule;

EMI or instalment details;

processing and other applicable charges;

applicable penal charges;

cooling-off or look-up period information for digital loans;

grievance redressal details.

Why APR matters more than the advertised interest rate

Suppose two lenders offer you a ₹5 lakh loan for three years.

Loan | Advertised Rate | Additional Charges | Practical Comparison |

|---|---|---|---|

Loan A | 12.5% | Higher processing and mandatory product costs | May have higher overall borrowing cost |

Loan B | 13.2% | Lower applicable charges | Could be cheaper overall |

Looking only at the nominal interest rate may make Loan A appear cheaper. APR is designed to give a broader annualised view of the cost of credit by incorporating applicable charges as prescribed.

For digital lending, RBI's guidance makes clear that applicable processing fees are included in APR calculations, and certain integrated insurance costs may also need to be included.

Borrower rule: compare the KFS and APR, not just the promotional rate or EMI displayed in an advertisement.

Transparent Loan Disclosures: What You Should Know Before Accepting

A compliant lending journey should reduce surprises.

Before accepting a loan, you should be able to understand:

the identity of the regulated lender;

the amount being sanctioned;

the applicable interest rate;

the APR;

the tenure;

the repayment frequency;

applicable charges;

conditions for prepayment or foreclosure;

consequences of delayed payment;

grievance redressal channels.

This transparency is particularly important in digital journeys because convenience can encourage fast decisions.

A message such as “₹5 lakh approved—complete now” is not enough information to evaluate a loan.

The approval amount tells you how much credit is available. It does not tell you whether borrowing that amount is appropriate for your cash flow or whether another offer has a better total cost.

A practical borrower test

Before accepting an offer, ask yourself:

If the promotional banner disappeared and I had only the KFS, repayment schedule and loan agreement, would I still take this loan?

If the answer is no—or if you cannot answer because the documents are unclear—do not rush the decision.

Digital Consent Is More Than Tapping “Allow”

One of the most important changes in responsible digital lending is the treatment of borrower data.

A loan application may genuinely require information for:

identity verification;

KYC;

fraud prevention;

income assessment;

bank statement analysis;

credit underwriting;

regulatory compliance.

But a loan app should not treat access to your entire digital life as a default condition of borrowing.

The regulatory approach requires data collection to be need-based, with explicit borrower consent and appropriate controls around collection, storage and use. The borrower should understand what information is being requested and why.

What meaningful consent should look like

A trustworthy journey explains the purpose of a permission before asking for it.

For example:

Clear consent

We need access to this document to verify your income for the loan application.

Questionable consent pattern

Allow all permissions to continue.

The difference is important. Consent should help the borrower make an informed choice; it should not simply remove friction from the lender's data collection process.

Before granting a permission, ask:

What data is being collected?

Why is it necessary?

Who is collecting it?

Will it be shared?

How long will it be retained?

Can I revoke consent where applicable?

Where can I read the privacy policy?

Data Privacy: A Loan App Should Not Need Your Entire Phone

One of the strongest borrower protections in the digital lending framework concerns unnecessary data access.

Borrowers should be cautious when a lending app seeks broad access to personal data that does not appear necessary for underwriting or servicing the loan.

Examples of warning signs include unexplained requests for broad access to:

contacts;

call logs;

photo galleries;

unrelated files;

other personal phone data.

A borrower should distinguish between legitimate verification and unnecessary digital surveillance.

For example, requesting a bank statement to assess income or cash flow can have a clear lending purpose. Asking for unrestricted access to unrelated personal information without a clear, proportionate explanation should raise questions.

This is particularly relevant for self-employed borrowers and MSMEs, who may share extensive financial information during underwriting. Business bank statements, tax documents and cash-flow information should be handled with the same discipline borrowers expect for personal data.

Responsible Lending May Mean More Checks, Not Fewer

Many borrowers assume that better digital lending rules should mean instant approval for everyone.

That is not the goal.

Responsible lending means using technology to make assessment faster and more accurate—not eliminating assessment.

A lender may examine factors such as:

verified income;

existing EMI obligations;

credit history;

repayment behaviour;

bank account cash flows;

employment stability;

business vintage;

turnover consistency;

existing debt obligations.

RBI has long emphasised realistic repayment schedules based on borrower cash flows, while fair-practice principles also focus on adequate disclosure and non-coercive recovery practices.

For borrowers, this creates an important distinction:

Fast approval is not the same as careless approval.

A lender asking for relevant documentation or verifying repayment capacity is not necessarily creating unnecessary friction. Those checks can be part of responsible underwriting.

How the Rules Affect Salaried Borrowers

For salaried individuals, digital underwriting can be relatively structured because income is often easier to verify.

A typical journey may involve:

PAN and identity verification;

KYC;

salary slips;

bank statements;

employment verification;

credit bureau assessment;

existing obligation analysis.

The most noticeable improvement for a careful borrower should be greater clarity around loan economics.

For example, imagine a borrower with a monthly take-home salary of ₹90,000 and existing EMIs of ₹25,000. An additional ₹30,000 EMI may look manageable during a good month, but the lender should consider repayment capacity rather than simply maximising the eligible amount.

The borrower should do the same.

Eligibility is a ceiling, not a recommendation.

A ₹10 lakh approval does not mean you should borrow ₹10 lakh if your actual requirement is ₹4 lakh.

How the Rules Affect Self-Employed Professionals

Self-employed borrowers often have irregular monthly income even when annual earnings are strong.

A consultant, doctor, architect or freelancer may earn ₹20 lakh annually but receive income unevenly. A salaried-style assessment based only on one month's inflow may not represent the borrower's actual financial position.

Digital lending can improve this process when lenders use relevant data responsibly.

Assessment may include:

income tax returns;

business or professional bank statements;

GST information where applicable;

invoice history;

average account balance;

business vintage;

existing liabilities;

seasonal cash-flow patterns.

The benefit is not necessarily instant approval. The real benefit is the possibility of a more accurate assessment using verified financial behaviour.

The borrower should therefore keep financial records organised before applying. Clean documentation can reduce back-and-forth and help the lender understand the true income pattern.

How the Rules Affect MSMEs

For MSMEs, borrowing decisions are rarely based on a single salary number.

A lender may need to understand:

business turnover;

cash-flow cycle;

GST filings;

bank statement patterns;

receivables;

existing facilities;

seasonality;

business vintage;

promoter profile;

intended use of funds.

RBI's MSME guidance notes that banks should assess genuine working-capital requirements while considering the business cycle and short-term credit needs. Current priority-sector rules also treat qualifying bank loans to MSMEs within the priority-sector framework, subject to applicable classification requirements.

For an MSME owner, this means the quality of the borrowing journey should be judged by suitability, not merely speed.

A three-year term loan may be appropriate for equipment expansion but unsuitable for a 60-day inventory cycle. Similarly, a short-tenure product may solve an immediate liquidity gap but create unnecessary repayment pressure if used for a long-term capital requirement.

Good credit advice begins with the purpose and cash-flow cycle of the borrowing need.

Compliant vs Non-Compliant Lending Journey: A Practical Example

Consider two borrowers applying for a ₹3 lakh personal loan.

Journey A: Transparent and borrower-centric

Meera applies through a digital platform.

Before accepting the offer:

She can identify the regulated lender.

She receives the KFS.

She can see the APR and applicable charges.

The data permissions requested are explained.

She reviews the repayment schedule.

The loan agreement and relevant documents are available to her.

Disbursement and repayment follow the prescribed lender-borrower flow.

She can identify a grievance redressal channel.

She understands the applicable cooling-off terms.

Even if the loan is not the cheapest in the market, Meera can make an informed decision.

Journey B: Warning signs throughout the process

Arjun sees an advertisement promising “₹3 lakh instant cash.”

The journey looks very different:

the actual lender is difficult to identify;

the app asks for broad phone permissions without clear explanation;

the advertisement focuses on the EMI but not the total cost;

applicable charges are unclear before acceptance;

the KFS is absent or difficult to access;

the repayment destination is confusing;

customer support information is vague;

pressure messages encourage immediate acceptance.

The issue is not simply that Journey B is less convenient or more expensive. The deeper problem is that the borrower cannot make a properly informed decision.

RBI's digital lending guidance is specifically structured around clearer disclosure, accountable lender-LSP relationships, controlled fund flows and borrower protections.

What Happens to Loan Approval Under the New Framework?

The regulations do not guarantee approval. They improve the framework within which a digital loan is offered and serviced.

A borrower may still be rejected because of:

insufficient repayment capacity;

high existing debt;

weak credit history;

unstable income;

unverifiable information;

inconsistent bank statement patterns;

internal lender credit policies.

The difference is that responsible lending should not be confused with indiscriminate lending.

For borrowers, the best preparation is straightforward:

check your credit profile before applying;

estimate an affordable EMI;

organise income documents;

avoid submitting unnecessary simultaneous applications;

compare total cost, not only approval speed;

borrow for a clearly defined requirement.

Will Documentation Become More Complicated?

Not necessarily.

Better regulation does not automatically mean more paperwork. In many cases, digital verification can reduce manual document handling.

However, faster documentation is not the same as no documentation.

KYC remains an important part of the lending process. RBI describes KYC as the process through which a regulated entity obtains and verifies information about identity, address, business nature and financial status as relevant to the relationship.

The exact documents required vary by product, lender and borrower profile.

A salaried applicant may commonly need salary and employment evidence. A self-employed professional may need tax returns and bank statements. An MSME may need business registration, GST-related information, financial statements and account data depending on the facility.

The better question is not:

Which lender asks for the fewest documents?

It is:

Which lender asks for relevant documents, explains why they are needed and provides a clear process?

How Repayment Is Becoming Safer and Clearer

A loan journey does not end at disbursement.

Borrowers should know:

the EMI amount;

due dates;

repayment method;

prepayment conditions;

applicable late or penal charges;

whom to contact during financial difficulty;

the grievance escalation process.

The digital lending framework also seeks to keep the flow of loan funds clear. RBI's FAQs state that a lending service provider should not handle funds flowing between the lender and borrower, subject to the framework's specified arrangements and exceptions.

This helps reduce ambiguity about where money comes from and where repayments go.

Borrowers should also understand the difference between penal charges and additional interest. RBI's fair-lending framework on penal charges was designed to prevent penalties from being used as a revenue-enhancement mechanism and to improve transparency in how charges for non-compliance are applied.

What Is the Cooling-Off Period?

Digital lending rules provide for a cooling-off or look-up period during which a borrower can exit a digital loan by paying the principal and proportionate APR without a penalty, subject to the applicable regulatory framework and disclosed terms.

A reasonable one-time processing fee may be retained if this was disclosed upfront in the KFS. RBI's digital lending FAQs explicitly clarify this treatment.

Why does this matter?

Digital interfaces can compress a major financial decision into a few taps. The cooling-off mechanism gives borrowers a limited opportunity to reconsider after disbursement.

Borrowers should check the applicable period in their loan documents rather than assume that every product has identical terms.

How to Identify a Trustworthy Lending Partner

A polished app, a large advertisement budget or a promise of fast approval does not prove that a lending journey is trustworthy.

Use this checklist before applying:

Identify the actual lender. Know which regulated entity will sanction and disburse the loan.

Read the KFS. Do not rely only on the EMI shown in an advertisement.

Compare APR and total repayment. A low headline rate can coexist with significant applicable costs.

Review data permissions. Ask whether each permission is necessary for the stated lending purpose.

Check repayment instructions. Understand whom you are paying and through which authorised channel.

Find the grievance mechanism. A legitimate journey should provide clear support and escalation information.

Avoid pressure-driven borrowing. Urgency is not a substitute for suitability.

Match the loan to the need. Tenure and repayment structure should reflect your income or business cash flow.

For borrowers who want help comparing debt structures rather than simply filling out multiple application forms, ExpressDhan positions its service around debt and structured-finance advisory, including personal, business and MSME borrowing requirements. Its most useful role in a regulated lending environment is not to promise that every application will be approved, but to help borrowers understand suitability, documentation readiness and lender-aligned execution.

Common Mistakes Borrowers Should Avoid in 2026

Choosing a loan only by EMI

A smaller EMI can result from a longer tenure and may increase total interest paid. Compare total repayment and APR.

Assuming “pre-approved” means guaranteed disbursement

A marketing offer may still be subject to verification, underwriting and lender policy.

Granting every app permission automatically

Read the purpose of each permission. Convenience should not require unexplained access to unrelated personal data.

Applying to too many lenders at once

Multiple applications can create unnecessary complexity and may result in repeated credit enquiries.

Borrowing the maximum eligible amount

The lender's maximum offer and your financially comfortable borrowing level are not the same thing.

Ignoring repayment flexibility

Before borrowing, understand prepayment terms, foreclosure conditions and the impact of late payments.

A Better Way to Compare Loan Offers

When comparing loans, use a simple decision framework:

Factor | Question to Ask |

|---|---|

Lender identity | Who is actually lending the money? |

Loan amount | Am I borrowing only what I need? |

APR | What is the annualised total cost measure disclosed? |

Total repayment | How much will I repay over the full tenure? |

EMI | Is it comfortable under normal and difficult months? |

Tenure | Does it match the purpose of the loan? |

Charges | Which applicable costs are disclosed? |

Data use | What information am I sharing and why? |

Prepayment | What happens if I repay early? |

Support | Who handles questions and complaints? |

This framework works for a ₹2 lakh personal loan and for a much larger MSME facility. The numbers change; the discipline does not.

What These Rules Mean for the Future of Borrowing

The direction of regulation is clear: digital lending in India is moving toward greater transparency, stronger accountability and more deliberate handling of borrower data.

That does not mean every loan will become cheaper.

It does not mean every application will be approved faster.

It does not eliminate the borrower's responsibility to compare offers and assess affordability.

What it can do is create a better decision environment.

The strongest borrowing journey in 2026 is not the one with the fewest screens. It is the one in which speed, transparency, privacy and suitability work together.

For salaried borrowers, that means understanding the real cost before accepting an offer.

For self-employed professionals, it means presenting a clear and verifiable picture of income and cash flow.

For MSMEs, it means choosing a credit structure aligned with the business cycle rather than accepting the first available facility.

And for every borrower, the principle is the same: know the lender, read the KFS, compare APR, protect your data and borrow according to repayment capacity—not merely eligibility.

Conclusion

RBI's digital lending framework is changing the standard borrowers should expect from an online loan journey.

A credible process should tell you who the lender is, disclose the cost of borrowing, provide key documents, explain data use, follow clear disbursement and repayment flows, and give you a defined path for resolving complaints.

The most important change, however, is behavioural.

Borrowers now have better tools to ask better questions.

Before your next personal, professional or MSME loan application, compare more than interest rates. Examine the structure of the loan, the quality of disclosure, the permissions being requested and whether the repayment obligation genuinely fits your cash flow.

Good borrowing decisions begin before the application is submitted.