A loan application is often decided long before you click “Apply.”

The months leading up to the application matter because lenders evaluate how you have managed credit over time: whether repayments were made on schedule, how heavily you depend on available credit, how frequently you apply for new loans or cards, and whether your overall debt appears manageable.

Your CIBIL Score is one of the most visible summaries of that behaviour. It is not the only factor a lender considers, and a high score does not guarantee approval. However, a stronger credit profile can improve your chances of qualifying for credit and may influence the terms available to you.

The good news is that credit health is not something you can only observe. Many of the behaviours that influence it can be improved.

The key is to start before you urgently need a loan.

This guide explains how a CIBIL Score works, what lenders actually look for, which actions can improve your credit profile, which popular shortcuts do not work, and how to prepare month by month before applying for a loan.

What Is a CIBIL Score?

A CIBIL Score is a three-digit numerical summary of an individual's credit history, ranging from 300 to 900. It is calculated from information in the credit report, including credit accounts, repayment behaviour and credit enquiries.

The score is provided by TransUnion CIBIL, one of India's credit information companies.

A simple way to understand the difference between a credit report and a credit score is this:

Your credit report is the record. Your credit score is a numerical assessment based on that record.

The report can contain information about:

active and closed loan accounts;

credit card accounts;

outstanding balances;

payment history;

overdue amounts;

lender enquiries; and

certain personal and account-related information reported by credit institutions.

It does not measure your wealth. A large bank balance, high-value investments or ownership of expensive assets does not automatically create a high CIBIL Score because savings, investments and fixed deposits are not part of the credit history used for the score.

Credit behaviour matters more than appearance of wealth.

For example, consider two borrowers.

Borrower A earns ₹2 lakh per month but frequently delays credit card payments and has applied for five unsecured loans recently.

Borrower B earns ₹80,000 per month, has manageable obligations and consistently pays every EMI and card bill on time.

Borrower A may have higher income, but Borrower B may demonstrate more predictable credit behaviour. A lender will evaluate the complete application, but income alone does not repair poor repayment history.

Why Your CIBIL Score Matters Before Applying for a Loan

Lenders use credit information to answer a practical question:

How risky is it to lend money to this borrower?

Your credit score helps with that assessment, but it should not be viewed as a universal approval or rejection number.

Different lenders have different underwriting policies. Depending on the product, they may evaluate:

credit score and detailed credit report;

income and income stability;

existing EMI obligations;

debt-to-income or fixed-obligation ratios;

employment or business stability;

loan amount and tenure;

collateral quality for secured lending;

recent credit applications;

internal lender risk policies; and

previous relationship with the lender.

This distinction is important because many borrowers focus exclusively on moving their score by a few points while ignoring larger problems in their application.

For example, someone may have a respectable score but already be using most of their monthly income for existing EMIs. Another applicant may have a good score but submit several loan applications within a short period. A third may have an error in the credit report that needs correction before applying.

A score is an important signal. The complete credit profile tells the fuller story.

What Influences Your CIBIL Score?

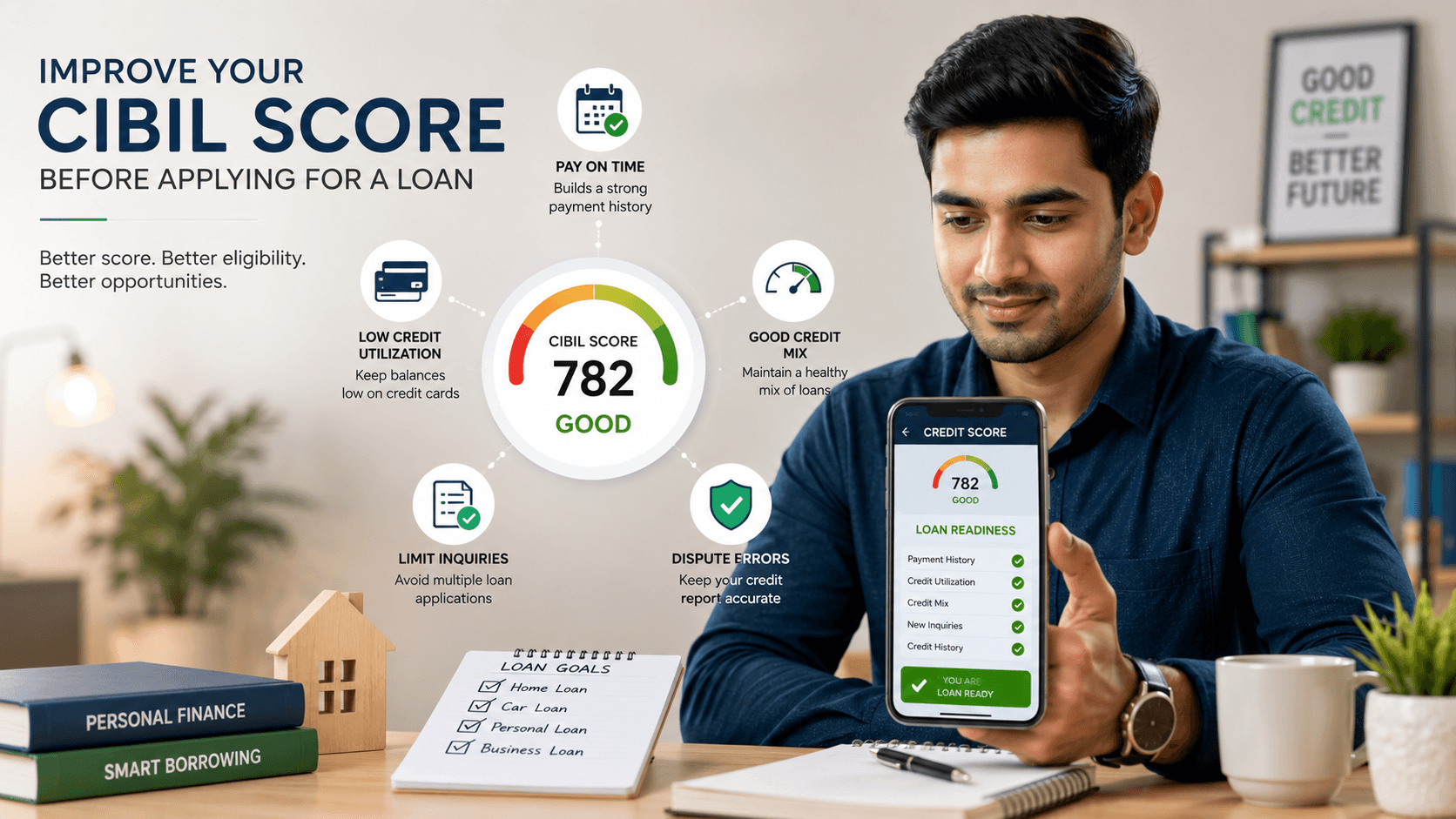

According to CIBIL's consumer education material, important factors include payment history, credit utilization, age or depth of credit and credit enquiries. The broader report also reflects the borrower's credit accounts and behaviour over time.

The exact score calculation is not something borrowers need to reverse-engineer. The practical goal is to understand the behaviours that strengthen or weaken a credit profile.

1. Payment History: The Foundation of Credit Health

If you remember only one rule, remember this:

Pay every EMI and credit card bill by the due date.

Late payments, missed payments and delinquencies can negatively affect the credit profile. Payment history shows whether a borrower has consistently met credit obligations as agreed.

Consider this example.

Riya has:

a personal loan EMI due on the 5th;

a credit card payment due on the 12th; and

a two-wheeler loan EMI due on the 20th.

She pays the personal loan and two-wheeler EMI on time but repeatedly forgets the card payment because she assumes one small delayed bill will not matter.

From a credit-management perspective, the problem is not simply the amount. Repeated delayed payment behaviour can signal unreliable repayment discipline.

How to reduce the risk of missed payments

Create a system rather than depending on memory.

Use automatic payments where appropriate, maintain enough balance in the repayment account before the debit date, and keep calendar reminders as a backup. Review statements regularly so that an incorrect transaction or unexpected charge does not remain unnoticed until the due date.

If cash flow is becoming difficult, address it before payments start failing. Cutting discretionary spending, avoiding new borrowing and speaking with the lender about legitimate available options is better than repeatedly ignoring due dates.

2. Credit Utilization: How Much of Your Limit You Use

Credit utilization refers to the proportion of available revolving credit that you are currently using.

Suppose your credit card limit is ₹1,00,000.

If your reported balance is ₹20,000, your utilization on that card is 20%.

If your balance is ₹85,000, utilization is 85%.

High utilization can make a borrower appear financially stretched. CIBIL advises consumers to keep utilization low, while its consumer education material has also described restricting card spending to around 30% of the available limit as a healthy practice.

The practical lesson is not to obsess over a magical percentage. It is to avoid routinely operating close to your credit limits.

A practical utilization example

Imagine that Arjun has two cards:

Card | Credit Limit | Current Balance |

|---|---|---|

Card A | ₹1,00,000 | ₹80,000 |

Card B | ₹50,000 | ₹10,000 |

Total | ₹1,50,000 | ₹90,000 |

His total utilization is 60%.

If Arjun is planning a home or personal loan application, reducing revolving balances can improve the appearance of his overall debt position. More importantly, it reduces expensive debt and creates additional financial breathing room.

The goal should not be to manipulate a score for a few weeks. The better objective is to demonstrate sustainable borrowing behaviour.

3. Credit Age: Why an Older Good Account Can Be Valuable

Credit history needs time to develop.

A borrower who has responsibly managed a credit account for several years provides lenders with more behavioural information than someone whose first account was opened recently.

CIBIL identifies age or depth of credit as one of the factors considered in a credit profile. A longer history of responsible management can indicate stability.

This is why closing your oldest credit card simply because you received a newer one is not always the best decision.

That does not mean every old account should remain open forever. A card with an expensive annual fee, poor terms or security concerns may deserve closure. The decision should consider cost, usability, repayment discipline and the effect on available credit—not a simplistic rule that old accounts must never be closed.

4. Credit Enquiries: Why Too Many Applications Can Hurt

When you apply for a loan or credit card, the lender may access your credit report. This creates a credit enquiry associated with the application.

A single enquiry is not a financial disaster. CIBIL states that such enquiries generally have a minimal or marginal impact, but frequent applications within a short period can negatively affect the credit profile.

The pattern matters.

Suppose you want a personal loan and submit applications to seven lenders over a weekend because you want to “see who approves first.”

From your perspective, you are comparing options.

From a risk perspective, multiple applications may suggest urgent demand for credit or the possibility of rapidly increasing debt exposure.

A better approach is to research eligibility requirements and likely terms before submitting formal applications. Compare first. Apply selectively.

Also review your report for enquiries you do not recognize. An unfamiliar enquiry deserves investigation rather than being ignored.

5. Secured and Unsecured Credit: Understanding Credit Mix

A secured loan is backed by an asset or security. Common examples include certain home loans and vehicle loans.

An unsecured loan is not backed by specific collateral. Personal loans and most credit cards are common examples.

CIBIL's educational material notes that a balanced mix of secured and unsecured credit may positively affect the credit profile, while excessive dependence on unsecured borrowing can be viewed less favourably.

However, this is frequently misunderstood.

Do not take an unnecessary loan merely to create a “better credit mix.”

Every loan creates a repayment obligation, potential interest cost and additional financial risk. Credit mix should develop naturally from genuine financial needs.

If you already have multiple personal loans and several heavily used credit cards, adding another unsecured account simply because an app offers instant approval is unlikely to improve your financial position.

How Lenders Evaluate Borrowers Beyond the Score

Many borrowers ask, “What CIBIL Score guarantees loan approval?”

The more useful question is:

What does my complete financial profile tell a lender?

A lender may examine whether:

your repayments have been consistently timely;

current debt is manageable relative to income;

card balances are repeatedly close to their limits;

several loans were opened recently;

there are unresolved overdue accounts;

your income can support the proposed EMI;

the requested loan amount is reasonable; and

your recent credit behaviour suggests stability or distress.

CIBIL itself notes that lender approval depends on multiple parameters and internal lender policies; a higher score improves credit readiness but does not guarantee approval.

Example: same score, different lending risk

Consider two applicants with similar credit scores.

Applicant 1

stable salary;

one existing vehicle loan;

low card balances;

no recent loan applications;

consistent payment history.

Applicant 2

similar salary;

three personal loans;

high card balances;

four recent credit enquiries;

no current late payment.

The numerical score may not tell you every detail of the difference between these profiles. A lender's underwriting process can.

That is why improving loan eligibility requires more than chasing a score.

How to Improve Your CIBIL Score Faster

There is no legitimate overnight method for rebuilding a credit history. However, you can stop avoidable damage immediately and improve the underlying profile systematically.

Pay overdue amounts first

If accounts are currently overdue, address them before experimenting with small optimization techniques.

A borrower with unpaid obligations should prioritize understanding:

which accounts are overdue;

how much is outstanding;

whether the reported information is accurate;

what can be paid immediately; and

what repayment arrangement, if any, is legitimately available from the lender.

Clearing an overdue amount does not erase the historical record of late payment. But continuing to miss payments adds new negative behaviour.

Reduce revolving credit balances

If cards are heavily utilized, create a repayment plan.

For example, if you have ₹1,20,000 in card balances across several cards, do not continue spending at the same rate while making only small repayments. Stop unnecessary new card spending and direct available surplus toward reducing balances.

The financial benefit can be more important than the score benefit: revolving credit can be expensive, and reducing the balance lowers future interest burden.

Stop unnecessary credit applications

If you are preparing for a major loan application, avoid applying for multiple cards, buy-now-pay-later credit lines or personal loans without a genuine need.

New credit should solve a real financial requirement, not satisfy curiosity about approval limits.

Keep good accounts healthy

A common mistake is focusing entirely on a past default while neglecting currently healthy accounts.

Every active EMI and card bill still needs to be managed correctly. Rebuilding is based on consistent behaviour across the profile.

Review the report, not just the number

A score tells you that something may need attention. The report helps you understand what.

Look for:

accounts that do not belong to you;

incorrect overdue amounts;

payments not updated correctly;

closed accounts still showing an inaccurate status;

duplicate accounts;

unfamiliar enquiries; and

incorrect personal information that could create identification issues.

How to Dispute Errors in a CIBIL Report

If your credit report contains inaccurate information, do not assume that waiting will automatically fix it.

CIBIL provides a dispute process for inaccuracies in a credit report.

A practical dispute process looks like this:

Obtain and review your latest credit report.

Identify the exact account, field or enquiry that appears incorrect.

Collect supporting records such as payment confirmations, closure letters or lender correspondence.

Raise a dispute through the appropriate official process.

Keep the dispute reference and supporting documentation.

Follow up with the relevant lender where necessary.

Review the updated report after the dispute process is completed.

A crucial distinction: you can dispute inaccurate information, but you cannot legitimately dispute accurate negative history simply because it is inconvenient.

If a late payment was correctly reported, the solution is not a false dispute. The path forward is to prevent new delinquencies and build a longer period of responsible behaviour.

CIBIL Score Myths That Can Delay Your Progress

Credit improvement attracts myths because borrowers naturally want quick solutions. Several of these myths can waste time or create additional debt.

Myth 1: Checking your own score lowers it

Reviewing your own credit information is not the same as repeatedly submitting formal loan applications to lenders.

The enquiries that deserve attention are those associated with applications for new credit. Regularly reviewing your report can help you identify errors or unfamiliar activity.

Myth 2: A high salary automatically creates a high score

Income and credit history answer different questions.

Your salary may affect repayment capacity and lender eligibility calculations. Your credit score reflects credit behaviour based on the information in your credit report.

A high-income borrower can still have poor repayment behaviour. A moderate-income borrower can maintain a strong record by borrowing within capacity and paying consistently.

Myth 3: Keeping a credit card balance improves the score

Carrying expensive debt is not a credit-building strategy.

Responsible card usage and timely payment can contribute to a healthy credit history. Paying interest unnecessarily does not prove that you are a better borrower.

Myth 4: Taking more loans improves credit mix

A balanced credit profile is not an invitation to manufacture debt.

Do not take a vehicle loan, personal loan or secured loan solely for the purpose of changing your credit mix. Borrow because the credit serves a legitimate financial objective and the repayment is comfortably affordable.

Myth 5: Closing every credit card improves your score

Closing cards can change available credit and may affect the depth of your credit history.

Evaluate cards individually. Consider annual fees, age of account, available limit, your spending habits and whether keeping the account open creates a risk of overspending.

Myth 6: A settlement completely solves the credit problem

A negotiated settlement and full repayment according to the original credit obligation are not necessarily viewed the same way in credit history.

Before accepting any settlement arrangement, understand the financial, contractual and credit-reporting consequences. Get terms in writing and confirm how the lender will report the account.

Mistakes That Can Cause Long-Lasting Damage to Borrowing Capacity

Some credit mistakes are temporary setbacks. Others can affect access to credit for a long time because negative repayment history does not disappear simply because the borrower now wants a new loan.

The most serious patterns include:

repeated EMI defaults;

prolonged credit card delinquency;

ignoring lender communication;

accumulating multiple high-cost unsecured debts;

borrowing to pay existing debt without solving the cash-flow problem;

acting as a co-borrower or guarantor without understanding the obligation;

repeatedly settling debts without understanding reporting consequences;

submitting numerous credit applications during financial distress; and

ignoring errors or unfamiliar accounts in the credit report.

The phrase “permanent damage” should be used carefully. A past mistake does not mean that a borrower can never rebuild. But accurate negative history cannot be instantly deleted through a trick, payment to a questionable “credit repair” service or a new credit card.

Rebuilding requires time and better subsequent behaviour.

How Long Does It Take to Improve a CIBIL Score?

There is no universal timeline.

A borrower with one reporting error may see improvement after the error is investigated, corrected and reflected in the report.

A borrower whose main issue is high card utilization may improve the underlying profile by reducing balances, although the visible score response depends on when updated information is reported and recalculated.

A borrower recovering from repeated defaults or serious delinquency should expect a longer rebuilding process.

A practical expectation framework is:

Credit Situation | What to Expect |

|---|---|

Incorrect information | Improvement depends on dispute resolution and reporting updates |

High card utilization | Profile may improve as lower balances are reported |

Too many recent applications | Stop new applications and allow time to pass |

Thin credit history | Build consistent behaviour over a longer period |

Repeated late payments | Recovery usually requires sustained on-time repayment |

Serious default history | Expect a longer rebuilding period; there is no instant repair |

Avoid anyone promising an exact score increase within a guaranteed number of days.

No legitimate adviser can guarantee that paying a particular amount today will increase a score by an exact number of points next month.

A Six-Month Credit Improvement Roadmap Before Applying for a Loan

If you are planning a significant loan application, preparation should ideally begin months in advance.

Month 1: Audit your complete credit profile

Obtain your credit report and examine every account.

Create a simple list containing:

lender name;

type of credit;

outstanding amount;

EMI or monthly payment;

due date;

account status;

utilization for cards; and

any reporting issue requiring investigation.

At the end of Month 1, you should know exactly what is helping and hurting your profile.

Month 2: Eliminate payment failures

Set up a reliable payment system.

Move due dates into a calendar. Maintain sufficient funds before automatic debit dates. Create reminders several days before each payment.

If any account is overdue, make it a priority according to your financial capacity and lender terms.

The objective for Month 2 is simple: no new missed payments.

Month 3: Reduce credit card dependence

Review card balances and identify avoidable spending.

Suppose your total limit across cards is ₹3 lakh and the outstanding balance is ₹2.1 lakh. Instead of applying for another card to create more available limit, focus on reducing the ₹2.1 lakh obligation.

Create a realistic repayment target that does not force you to borrow elsewhere for essential expenses.

The goal is sustainable reduction, not temporary repayment followed by immediate re-spending.

Month 4: Stabilize the profile

Do not make unnecessary applications for new credit.

Continue:

paying every obligation on time;

reducing revolving balances;

checking lender statements;

following up on unresolved report disputes; and

keeping monthly debt obligations under control.

This month may feel uneventful. That is useful. Creditworthiness is built through predictable behaviour, not constant financial activity.

Month 5: Test loan affordability

Before applying, calculate whether the proposed EMI fits your real budget.

Do not use only the lender's maximum eligibility.

Ask:

How much income remains after existing EMIs?

Can I pay the new EMI while maintaining emergency savings?

What happens if a bonus or variable payment does not arrive?

Can I manage the EMI if major household expenses increase?

Am I relying on credit cards to fund regular monthly expenses?

A loan that is technically approved can still be financially uncomfortable.

Month 6: Review and apply selectively

Review your latest available credit information and confirm that:

there are no unexpected overdue accounts;

card balances are under better control;

recent applications have been limited;

disputes have been followed up;

your proposed EMI is affordable; and

documents required for the loan are ready.

Then compare lenders and apply selectively rather than sending applications everywhere at once.

A Practical Example: Rebuilding Before a Personal Loan

Consider Neha, a 29-year-old professional planning to apply for a personal loan.

Her initial situation is:

monthly take-home income: ₹90,000;

vehicle EMI: ₹12,000;

two credit cards with combined limits of ₹2,00,000;

total card balance: ₹1,25,000;

one delayed card payment several months ago;

three recent loan enquiries.

Her first instinct is to apply to more lenders until one approves her.

A better plan is different.

First, she stops submitting new applications. She reviews her credit report to ensure that all accounts and enquiries are accurate. She automates the vehicle EMI and card payments to prevent new delays. Over several months, she reduces her card balances and avoids replacing repaid debt with new spending.

She also evaluates the proposed personal loan EMI against her existing ₹12,000 vehicle obligation and normal living expenses.

The important improvement is not merely a different number on a screen.

Her financial profile becomes easier to explain:

stable repayment behaviour;

lower dependence on revolving credit;

fewer recent applications;

manageable existing obligations; and

a loan request supported by realistic repayment capacity.

That is what credit preparation should achieve.

What First-Time Borrowers Should Do Differently

A first-time borrower may have limited or no established credit history. This is different from having a history of poor repayment.

The objective should be to build credit gradually and responsibly.

A sensible approach is to:

take credit only when there is a genuine need;

start with obligations that are comfortably manageable;

pay every amount on time;

avoid opening several accounts simultaneously;

understand billing cycles and due dates;

review credit reports periodically; and

treat a credit limit as a maximum facility, not a spending target.

The worst approach is to borrow aggressively simply to create a credit history quickly.

A thin file needs responsible history, not maximum activity.

What to Do If You Are Recovering From Financial Setbacks

Recovery should begin with cash flow, not score obsession.

List every debt and classify it by:

current or overdue status;

outstanding balance;

interest cost;

monthly payment requirement;

secured or unsecured nature; and

immediate consequence of non-payment.

Then create a realistic repayment plan.

If your current income cannot support existing obligations, adding new debt to improve a score is unlikely to solve the underlying problem.

Focus first on preventing the situation from worsening:

stop unnecessary borrowing;

prevent new missed payments where possible;

communicate with lenders through official channels;

retain payment and correspondence records;

verify how accounts are being reported; and

build a sustainable budget.

CIBIL's own consumer education emphasizes that rebuilding a low score is based on clearing outstanding obligations where possible, keeping balances lower, applying for new credit cautiously and maintaining good repayment behaviour over time.

A Pre-Loan Credit Checklist

Before submitting an important loan application, confirm the following:

I have reviewed my credit report, not only the score.

All accounts on the report belong to me.

I understand the status of every overdue or previously delinquent account.

I am paying all current EMIs and card bills on time.

My credit card balances are under control.

I have not made unnecessary recent credit applications.

My proposed new EMI fits comfortably within my monthly budget.

Any inaccurate information has been disputed through official channels.

I have compared loan terms before making formal applications.

I am not depending on a guaranteed score increase or instant credit-repair promise.

If several answers are “no,” delaying the application may be more valuable than searching for another lender.

Conclusion: Build Loan Eligibility, Not Just a Number

Improving your CIBIL Score is not about finding a loophole in a scoring system. It is about creating a credit profile that shows consistent repayment, controlled borrowing and financial stability.

The fastest useful improvements usually begin with straightforward actions: stop missing payments, reduce excessive card balances, avoid unnecessary credit applications, investigate report errors and give responsible behaviour enough time to become part of your credit history.

For someone applying for a first loan, the goal is to build a clean and manageable credit record from the beginning.

For someone recovering from past setbacks, the goal is to stop adding new damage and establish a sustained pattern of better behaviour.

And for anyone planning a major loan, the most important lesson is simple: credit readiness should begin months before the application, not after the rejection.

A better score can strengthen your position, but the real objective is broader—becoming a borrower whose income, obligations and credit behaviour together support responsible approval.